2022 year-end digital health funding: Lessons at the end of a funding cycle

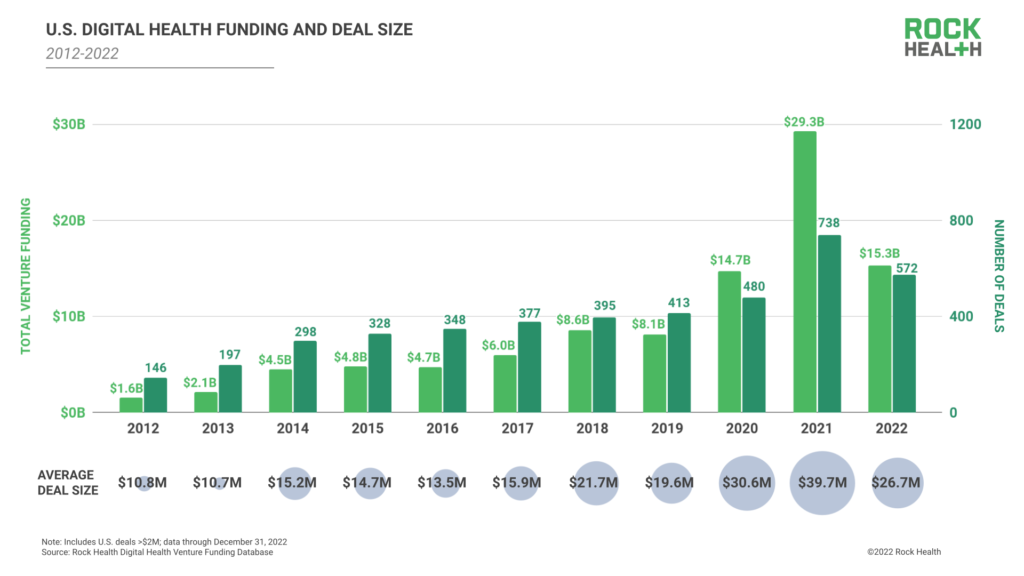

Ahh, 2022: the year of inflation, stock drops, and a whopping seven (7!) interest rate hikes that cozied us up to the possibility of recession. In this period of difficult economic changes, much of digital health’s “up” came down (see: unicorn stumbles, big ticket IPO tanks). Overall, U.S. digital health funding scraped by with $15.3B, underperforming 2021’s pot and just beating out 2020’s total.

For the digital health sector, 2022 was a downhill ride—one that we think signals the tail end of a macro funding cycle centered around the COVID-19-era investment boom. But downhill paths carry both positive and negative connotations, and the following lessons from 2022 can help to make the most of the current market:

- As a three-year digital health “funding cycle” comes to a close, the investment market will recalibrate to a more sustainable run rate.

- In the current VC climate, strong horses will beat out unicorns…though investors run the risk of betting on the wrong equine.1

- While diminishing margins have forced big healthcare organizations (especially health systems) to focus on near-term needs, successful players will continue to plant seeds for better seasons.

- “Disrupting” healthcare isn’t as effective as targeting transformation opportunities in tried-and-true operational fields—a lesson Big Tech learned all too well.

- We’ve all been reminded that you can’t fight Mother Nature (aka macroeconomic forces), with D2C startups bearing the brunt of the reminder.

Read on for our analysis of 2022’s biggest digital health moments and trends, plus takeaways to make for a smoother slide into 2023.

2022: What really happened

2022’s total funding among US-based digital health startups amounted to $15.3B across 572 deals, with an average deal size of $27M. Not only did 2022’s annual funding total come in at just over half of 2021’s $29.3B2, but it also just squeaked past 2020’s $14.7B sum. Notably, 2022’s year’s Q4 $2.7B total was less than half of last year’s Q4 raise ($7.4B).

Within digital health and in capital markets more broadly, we’ll likely look back on the past several quarters as a macro funding cycle. Between Q3 2019 and Q2 2021, investors continuously increased investments into digital health quarter-over-quarter for seven straight quarters, with one dip in Q2 2020. On the way down from the Q2 2021 peak to present day, investors steadily decreased the flow of capital every quarter, excluding two quarterly upticks: one in Q4 2021 and a smaller notch in Q4 2022.

Drivers toward this cycle’s “crest” in mid-2021 have been well documented. The COVID-19 pandemic catalyzed digital health innovation, investment, and regulatory reform throughout 2020 and 2021. Intertwined with the public health emergency, government stimulus measures contributed to an artificially depressed cost of capital in 2020-2021, encouraging investors to make bigger and riskier bets in emerging areas like digital health. As a cherry on top, 2021 saw the Fed underestimate percolating inflationary concerns and extend monetary easing measures, inflating asset prices and valuations.

In late 2021 and early 2022, what went up started to come down. Supply chain challenges, inflation, interest rate hikes,3 and investor pullback reversed investment momentum. H2 2021 averaged $7.1B in quarterly funding, a small decline from the first half of that year. In 2022, the rate of decline accelerated: H1 2022 averaged $5.2B in quarterly funding, and in H2 2022 average quarterly funding fell to $2.4B. To illustrate the slope of change, Q4 2022’s $2.7B in funding sits 68% lower than Q2 2021’s summit.

It’s too early to say whether we’ve reached the end of this macro funding cycle, or if more low funding quarters are on the horizon. With recession concerns looming, H2 2022’s quarterly average of $2.4B may be a bellwether for the next several quarters—which means that 2023 could be digital health’s first $10B or lower year in venture funding since 2019. However, there are signals that funding could start to inch back up again: investors have dry powder stockpiled, and difficult exit climates are likely to draw late-stage digital health companies back to the fundraising table. Whenever investment starts to pick up again, digital health’s next growth trajectory will look more like 2011-2019 than 2019-2021—a slower and more sustained path that better reflects startup risk and prioritizes companies taking measured paths to success.

Thinning out the unicorn herd

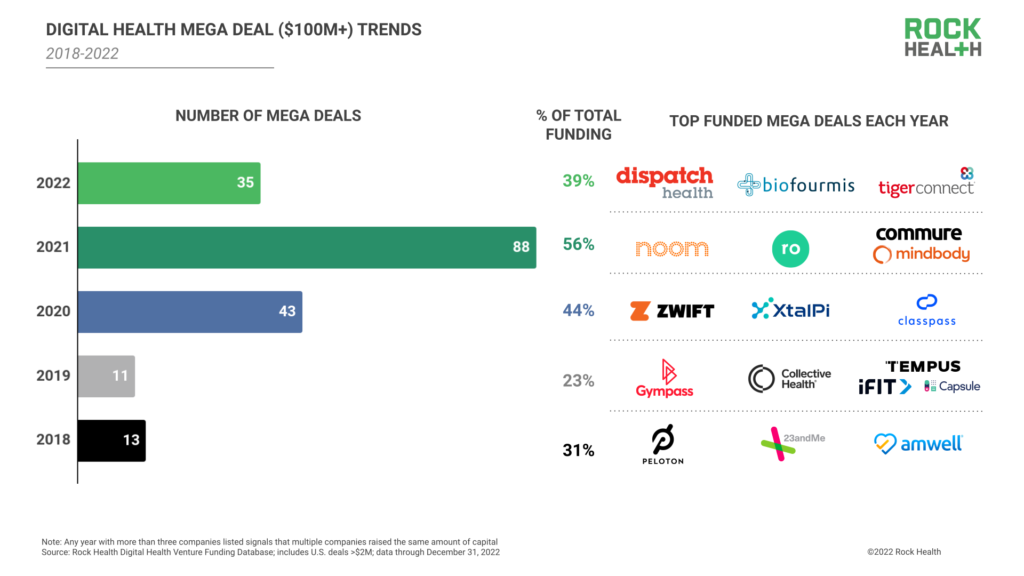

A notable contributor to 2022’s “downhill” funding trajectory was investors’ reluctance to invest heavily in late-stage deals, leading to a dearth of mega deals relative to prior years. In 2022, 35 digital health startups raised rounds of $100M or more. While this may sound like a hefty cohort, it pales in comparison to the volume of mega-rounds raised in 2021 (88) and even 2020 (43). This marked a reversal in capital concentration (a funding environment where late-stage companies attract a disproportionate share of total dollars invested), a phenomenon prevalent in digital health from 2019-2021.

As we’ve shared before, some of 2022’s “missing” mega deals stemmed from growth-stage digital health companies’ reluctance to raise in this market environment for fear of the dreaded down round. Additionally, startups that once expected to mega-raise their way into the unicorn club were faced with investors who were less willing to take flights of fancy on $1B valuations; as a result, they may have chosen to delay big raises.

For growth-stage startups that didn’t raise in 2022, limited cash reserves may push once-crowned digital health unicorns back to the fundraising table (possibly at lower valuations) or toward M&A territory. 2023 will likely see some “fallen” unicorns accept acquisition bids if cash reserves are short. For those that choose to pursue investment instead of M&A, grounded approaches will be the most successful. Investors are wary of unicorns’ spells, but they’re on the lookout for strong horses: startups that don’t rely on the promise of magical growth but are instead grounded in demonstrated cost savings, clinical workflow improvements, and interest from market buyers.

“A few months ago, it was detrimental for a digital health startup to say it was profitable—it implied the company wasn’t growing fast enough. Now, startups with strong financials and balanced valuations are attracting investor and acquirer interest.”

— Ulili Onovakpuri, Managing Partner, Kapor Capital

For strong performers, valuation risks remain in early stages

Investors interested in strong horses spent 2022 scoping out earlier-stage opportunities. Two quarters ago, we noted a shift in investors’ attention from growth-stage players to early-stage digital health companies perceived as less likely to carry inflated valuations from 2020-2021. As investors competed to back early-stage prospects, Series A deals got bigger than ever before. The median check size for Series A deals reached an all-time high of $15M in 2022, while median deal sizes shrunk across all other later deal stages.4

The movement of bidding wars from growth-stage deals to Series A rounds doesn’t eliminate valuation inflation overall—instead, it shifts inflated prices upstream. By competing in earlier rounds, investors are more likely to pay more on a risk-adjusted basis for a startup than its later-stage funders, twisting the risk-adjusted valuation upside down. In a market where late-stage transaction volume has plummeted, we anticipate that 2022’s cohort of larger Series A deals may experience above average value attrition, risking down rounds at their Series B raises or later.

Balancing frontline and frontier innovation

In a year of roadblocks, big health players were pushed to implement near-term solutions while still stretching to keep eyes on the innovation horizon. Particularly for health systems, 2022 may be remembered as the year things went upside down. Excluding COVID-19 and behavioral care visits, patient encounters were 6.2% lower compared to early 2019, suggesting that some patients permanently forwent pandemic-delayed care. Staffing crises and wage inflation hiked up operating costs faster than CMS-influenced rate adjustments, squeezing health system margins rather than allowing hospitals to pass costs through to payers. As a cherry on top, burnout pushed record numbers of clinicians to retire or work fewer hours, which kept health systems in crisis mode…and paying crisis wages. With all these forces compounded, several hospitals across the U.S. recorded losses of over one billion dollars in 2022.

For health systems, a top 2022 priority was identifying immediate steps to stop the bleeding (healthcare pun intended). In addition to taking traditional expense reduction efforts and charging new fees, hospital systems evaluated nonclinical and clinical workflow improvements to unlock efficiency gains and reduce provider pain points at work. Forty-five percent of provider organizations reported accelerating their software investments in 2022 to streamline operations.

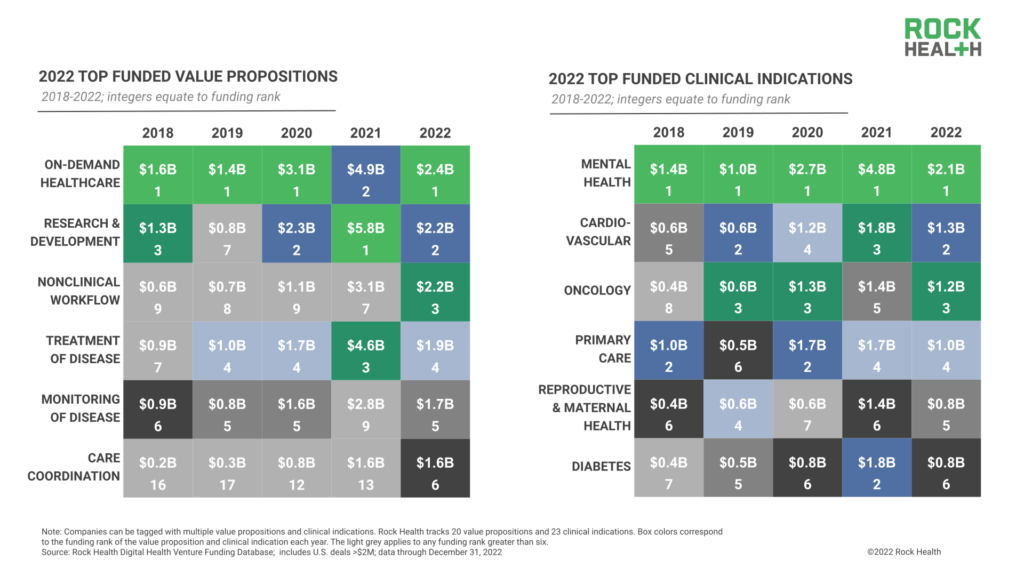

The front-and-center focus on efficiency gains boosted investment for nonclinical workflow solutions. Funding for this value proposition earned third place in 2022 ($2.2B), jumping from seventh place in 2021. And clinical workflow software, which earned eighth place in 2022 ($1.5B), moved up from eleventh in 2021. Besides investments, health systems pursued long-term partnerships with software providers to make efficiency inroads, such as Cleveland Clinic’s 10-year deal with Palantir to roll out AI solutions that better forecast and manage patient flows.

“Health systems are looking for digital solutions that are easy to understand, can be deployed relatively quickly, and deliver tangible cost savings and efficiencies. We need to find ways to help health systems reduce admin burden and free up clinician time.”

— Navid Farzad, Partner, Frist Cressey Ventures

Health systems also took steps to shift toward care models that decrease operational burden. Ambitious hospital–at–home initiatives were launched to free up hospital beds, allow top of license practice, and reimagine care pathways. Mass General Brigham announced plans to grow its hospital-at-home programs from 25 patients to 200 over the next two years, while 12-hospital health system Allina Health partnered with Flare Capital Partners to spin out hospital-at-home company Inbound Health ($20M), delivering extra-clinical care across 185 different diagnoses. Seizing the opportunity, startups in the on-demand care space like TytoCare emphasized their role to play in hospital-at-home programs. In part because of hospital-at-home excitement, on-demand healthcare landed the top-funded digital health value proposition spot of 2022 ($2.4B), led by urgent-care-at-home service DispatchHealth ($330M) and startups like Homeward Health, which raised twice in 2022.

In addition to dealing with frontline priorities, 2022 saw key health systems continue to carve out brainspace to expand and explore new businesses that would diversify revenue streams in years to come—an important balance even as tough times bias toward short-term solutions. Provider venture capital funds remained the top corporate investors by deal volume, and provider organizations increased their acquisitions by 5x, from three deals in 2021 to 15 in 2022 (acquisition targets included specialty care coordinators and telemedicine startups). Health systems also established partnerships as first steps into new revenue or equity pathways, shaking hands with venture capital teams like General Catalyst and a16z to establish digital health startup pilot sites on hospital campuses.

It’s worth calling out that competition is a powerful motivator for health system innovation, especially as retail giants battle their way into care delivery. In the early innings of retail care, questions were raised about the quality of care being delivered; however, access-related benefits for patients and heavy internal and external investment activity suggest that care delivered in the retail setting is here to stay. Big H2 2022 splashes from retail giants Walmart and Walgreens have raised the stakes for primary care, at-home, and omnichannel care delivery expansion. Health systems strategizing for the years ahead are coming to realize that their beyond-the-hospital care offerings must stand up to a growing pool of competitors.

Health systems’ 2022 innovation “grace under pressure” is noteworthy and sets a precedent for other major healthcare companies facing less difficult, but nonetheless challenging situations. For employers, health plans, and life science firms bracing for cost challenges or new mandates in 2023—not to mention the impending end of the COVID-19 public health emergency—we hope health systems’ 2022 moves set the tone for all enterprises balancing the immediate with long-term innovation decisions.

Big Tech reorients healthcare initiatives

Health systems weren’t the only ones facing uphill battles in 2022. Volatile active user numbers and declining profitability due to weakened advertising revenue deeply depressed Big Tech stock prices, and we expect that these pressures will further push the MAMAA crowd toward new revenue opportunities outside of tried-and-true social media advertising. Last year’s efforts to diversify revenue streams saw Big Tech players building up businesses in data infrastructure, analytics, and finance, not to mention taking on the challenge of healthcare innovation in earnest.

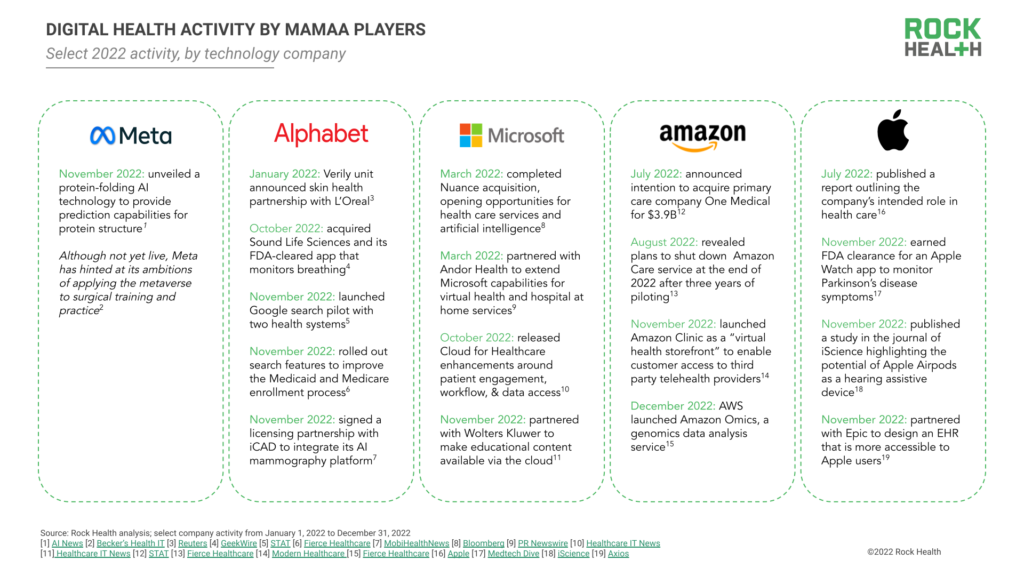

At the beginning of 2022 when Big Tech companies were awash in cash reserves, MAMAA players propped up internal healthcare experiments and waded into new territory with partnerships and acquisitions. But as the year unfolded and cash grew costly, several of these health experiments were scrutinized, discontinued, or divested. Adopting a more conservative mindset, Q4 2022 saw Big Tech players recenter digital health strategies within their tried-and-true operational fields. Amazon leveraged its experience creating and scaling two-sided marketplaces to launch Amazon Clinic, a virtual health storefront offering access to third-party telehealth providers. Google returned to its roots and unveiled several medical search initiatives for clinicians and consumers. Meta applied its artificial intelligence chops to protein folding, and Apple invested in proving out the clinical fidelity of its wearable devices.

What’s 2022’s takeaways for MAMAA, other Big Tech players (e.g., Netflix, Nvidia, Samsung), and middle children? The best healthcare entry points exist where teams already hold expertise (fertile ground remains in these familiar pastures). Rather than aiming to “disrupt” the entire healthcare system, focus is best placed on applying practiced skill sets to top healthcare and research problems. Finally, it’s important to draw boundaries between conflicting business units—probably best to steer clear of mixing healthcare and consumer marketing, and focus instead on cloud hosting and patient data interoperability.

Macro conditions ding D2C startups

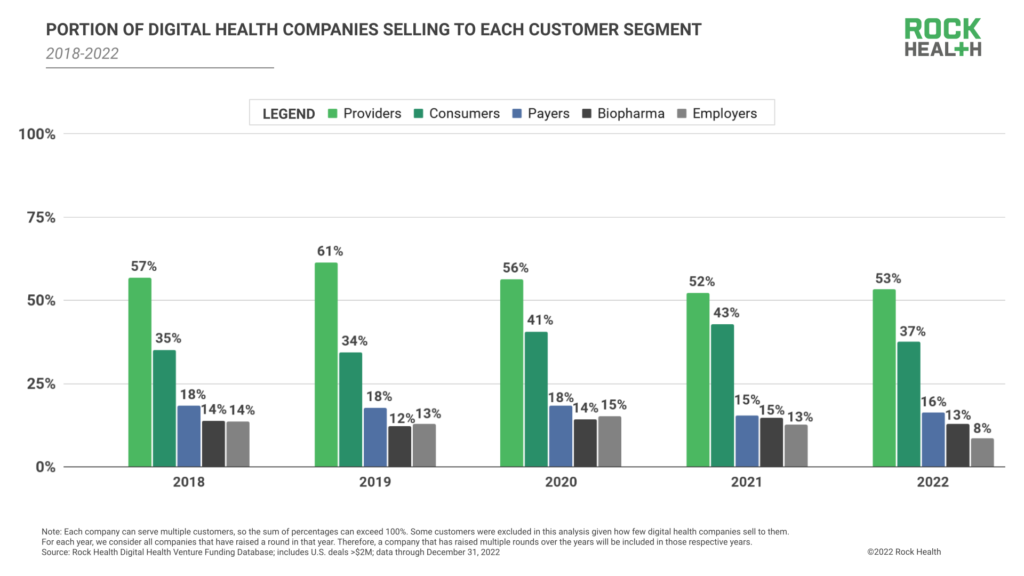

We ended 2021 reflecting on the rise of digital health solutions selling direct-to-consumer (D2C), as increased out-of-pocket healthcare spend gave startups consumer dollars to aim for. However, 2022 didn’t go as well for D2C digital health players, with only 37% of the digital health companies that raised in 2022 selling directly to consumers, compared to 43% in 2021.5 Not to mention, D2C stocks felt crushing pressure in the public markets—and not just in the healthcare industry. Several D2C digital health equities including Peloton (-78%), Owlet (-79%), and Beachbody (-78%) ended the year at fractions of their 2022 opening prices.

For D2C startups, 2022’s Achilles’ heel was rooted in larger economic forces, rather than sector-specific factors. Inflationary pressures burned consumers’ discretionary dollars. Mobile privacy updates gave way to rising customer acquisition costs (CAC); for some D2C digital health startups, CAC is estimated to have rocketed from $150 in 2018 to $500-$1,000 in 2022. Not to mention, conservative VC activity shortened cash runways. Especially for young D2C digital health entrants that needed to invest heavily upfront to establish brand recognition and consumer leads, last year’s unfavorable macro conditions raised roadblocks for market penetration.

In the absence of cheap cash to purchase consumers or a captive audience of pandemic-time buyers, D2C companies were forced to look hard at operational efficiency and customer lifetime value. Some players differentiated through new features, product category expansions, and forged partnerships to enhance consumer value. Others expanded their revenue potential by diversifying into B2B. Noom and Oura targeted employers interested in modernizing health and wellness benefits, Calibrate sought out payer reimbursement, and Whoop explored applications in remote monitoring.6

“D2C businesses that have established strong consumer DNA and proven unit economics could be well-positioned to add more healthcare services under their brand umbrellas.”

— David Kopp, Executive Chair, Oar Health

Given the current economic situation, it’s possible that consumers will spend even more conservatively in the months ahead—which means that macro headwinds for D2C won’t be relenting. For some D2C players, differentiated tech and/or B2B sales will help to deflect bottom-line impact. For others, 2023’s continued pressures might be a final nail in the coffin, with shuttered doors or acquisitions on the horizon.

WANT TO SHARE THESE INSIGHTS WITH YOUR TEAM? ACCESS ROCK HEALTH’S 2022 RECAP SLIDES HERE

Conclusion

In a downtrodden market climate, things don’t need to feel doom and gloom. 2022 was a necessary reminder that investment is cyclical, and that strong players build resilience in weathering funding climate changes. We expect that 2023 will be built up on slow, steady, and maybe even boring strategies for healthcare startups and enterprises alike: managing cash, re-structuring to accommodate revenue volatility, and investing in technology infrastructure. But spring is on the horizon. Digital health can’t “cut” its way to impact, and the smart decisions of today will fertilize the next investment upswing.

Rock Health Capital continues to invest in early-stage entrepreneurs bringing unique and innovative technology to healthcare. We would love to hear from you. Get in touch!

Rock Health Advisory provides guidance on digital health strategy, access to proprietary funding data, and in-depth perspectives on the digital health market. For digital health insights targeted to your needs, drop us a note.

Finally, stay up to date with the latest headlines in healthcare technology and Rock Health news by subscribing to the Rock Weekly.

Footnotes

- Though a source of some internal controversy, it is nonetheless Rock Health’s official position that both unicorns and horses share the genus Equus.

- Rock Health’s databases are continuously assessed and updated as new information becomes available. For this reason, data quoted in this piece may differ from prior Rock Health pieces due to updated information in our databases.

- In our 2019 year-end report, we predicted that “shockwaves of an economic slowdown would ripple into the private markets,” as a 10-year bull-run in capital markets came to an anticipated close. We were only off by three years—aka one pandemic.

- Given that deal size generally tracks to valuations, it’s fair to infer that the median Series A deal valuation is likely at or near all-time highs.

- This percentage includes digital health companies that sell exclusively to consumers, as well as those that sell to consumers in addition to other customer types (e.g., employers, providers, payers).

- Adoption of B2B models doesn’t necessarily change a D2C company’s customer-centricity. As a16z recently mused, a health company doesn’t need to be D2C to be consumer-minded; the value of patient-centered design can carry across business models.