2024 year-end market overview: Davids and Goliaths

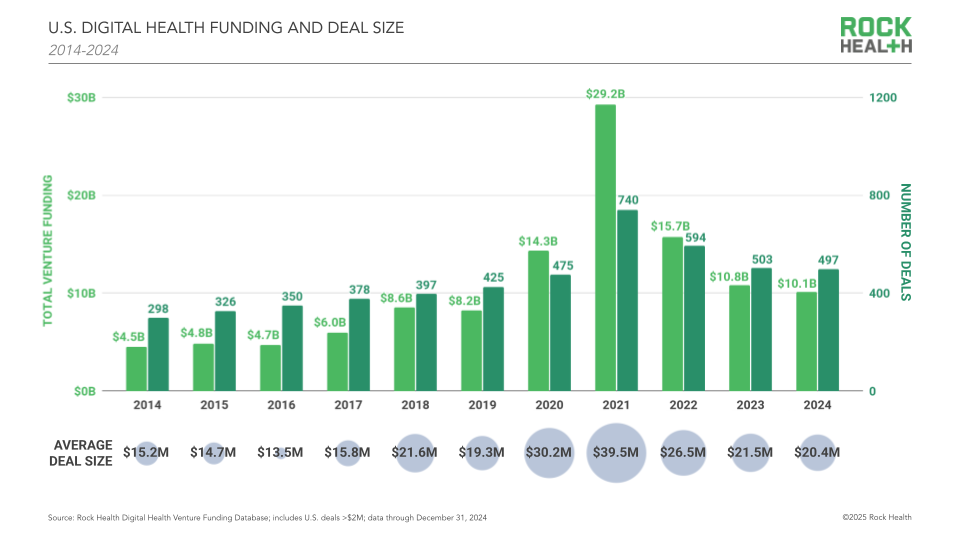

As we embark on the new year, we’re taking a moment to reflect on the trends and activity that shaped digital health and healthcare innovation in 2024. Venture funding for U.S. digital health startups totaled $10.1B across 497 deals this year, after logging $1.8B across 118 deals in Q4. 2024’s lower funding pot was influenced by investors’ focus on earlier-stage funding, as well as a pullback on later-stage check sizes.

While 2024 saw heightened earlier-stage investment activity, a handful of large, more established players dominated healthcare innovation headlines. Heavyweight investors drove sector dealmaking, with mega funds like Andreessen Horowitz and General Catalyst leading the charge in digital health by transaction count. Big Tech players commanded the foundation model front, and a few companies competed to be AI partners for the nation’s largest healthcare organizations. Funding concentrated into already popular value propositions and therapeutic areas, including nonclinical workflow, mental health, and obesity care.

These dual trends—early-stage startup activity amidst big moves by large healthcare players—have created a David and Goliath dynamic in the healthcare innovation landscape. We see a future where David and Goliath can coexist, and even thrive together, to drive impactful change in healthcare. Achieving this vision will require that all parties understand their roles and opportunities for symbiotic relationships in the market.

2024 market overview

Annual venture funding in digital health totaled $10.1B across 497 deals, reflecting a slight decrease from 2023’s total dollars and a nominal decline in number of deals.

While 2024 outperformed the $8.2B raised in 2019 (our benchmark year outside of the COVID-19 funding cycle) in absolute terms, adjusting for inflation changes the story. One U.S. dollar in 2024 was worth approximately $0.82 in 20191—meaning that 2024’s $10.1B in digital health funding approximates to only $8.3B in 2019 dollars, nearly identical to 2019’s actual amount of capital raised.

There are a few contributing factors to lower funding levels in 2024 compared to prior years. One was investor focus on earlier-stage dealmaking, continuing a trend we saw in 2023. Sixty-three percent of 2024’s funding rounds were labeled2 (an uptick from 57% in 2023), and, of these labeled deals, 86% supported startups raising their Seed, Series A, and Series B rounds. Investors are betting on younger companies, some of which are free from the valuation baggage of 2020-2022 fundraising.

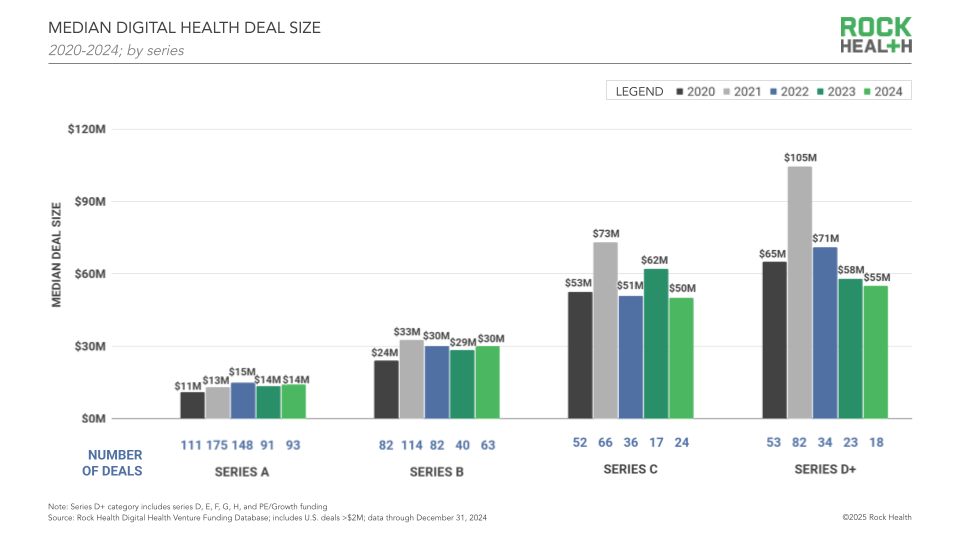

Another contributing factor to 2024’s smaller pot: digital health companies that raised later-stage rounds in 2024 did so at smaller check sizes compared to previous years. Median deal size for Series C and D fundraises clocked in at $50M and $55M respectively—drops from 2023’s $62M and $58M, and big slashes from 2021 highs of $73M and $105M. 2024’s decline in later-stage funding also corresponds with a decline in mega deals, or fundraises over $100M. 2024 saw fewer mega deals (17), accounting for 21% of the year’s overall sector funding—continuing a decline from 32% in 2023, 38% in 2022, and 56% in 2021.

Increasing early-stage fundraising activity, alongside smaller late-stage deals drove 2024’s total funding numbers downward—a dynamic that gives us important intel as we head into 2025. New startups are attracting investor attention despite a more tempered funding environment; yet, as we’ll discuss later on, their growth trajectories will depend on how effectively they navigate a Goliath-rich environment. Later-stage startups struggling with downward valuation pressures or stalled fundraising rounds could fold or seek acquisition in the coming year—potentially restarting digital health M&A activity, which hit a decade low in 2024 at 118 deals.

“Many late-stage players spent significant capital developing and piloting their solutions, but weren’t able to clear the necessary hurdles to operate sustainably at scale. Today’s decrease in late-stage investments will likely lead to more M&A in the near future. These acquisitions may not be ‘champagne popping’ events, but they will streamline operations and free up founders to eventually start a new crop of digital health companies.”

– Lawrence M. Chu, Co-Chair of Global M&A, Goodwin

Navigating investment in the world of mega funds

We can’t talk about 2024’s digital health funding landscape without mentioning a broader trend in venture capital: deployable capital is becoming increasingly concentrated among a select group of investor heavyweights. According to research from Pitchbook, of the 391 VC firms in the U.S. venture market, 30 funds raised 75% of all of 2024’s committed capital in the U.S., and just nine of those funds accounted for 50%.3

Top VC firms with at least $500M to deploy are often referred to as “mega funds.” Two well-known mega funds—Andreessen Horowitz (a16z) and General Catalyst (GC)—together captured 20% of all committed LP capital in the U.S. venture market this year. These two funds also led the charge in digital health investment. A16z and GC were the sector’s top investors in 2024, based on disclosed investor syndicates.

Large coffers and brand recognition put mega funds like a16z and GC in unique positions to shape the future they’re betting on. A16z has used its wide-reaching brand platform to call attention to the transformative potential of AI, priming the market for the AI startups it’s funding in healthcare. GC positions its portfolio companies for success by facilitating synergies across key healthcare partners and assets. From acquiring a health system via its company Health Assurance Transformation (HATCo) to forming symbiotic relationships with national healthcare partners like HCA, GC carves out “test drive” opportunities for its investments. Mega funds can also provide capital for their port cos to acquire other players, consolidating influence within key sector categories.

Mega funds are doing big things to transform healthcare, and their growing influence adds a new dynamic to startup relationships. For startups, it’s important to recognize differences between David and Goliath investors and understand the value of working with each. Mega funds can draw market attention and open doors to worthwhile partners, but can also influence deal terms and alter company trajectories. Ultimately, knowing what you’re looking for in terms of capital, terms, and strategic support will help determine which funds are best to have on the cap table.

The LLMs in the room

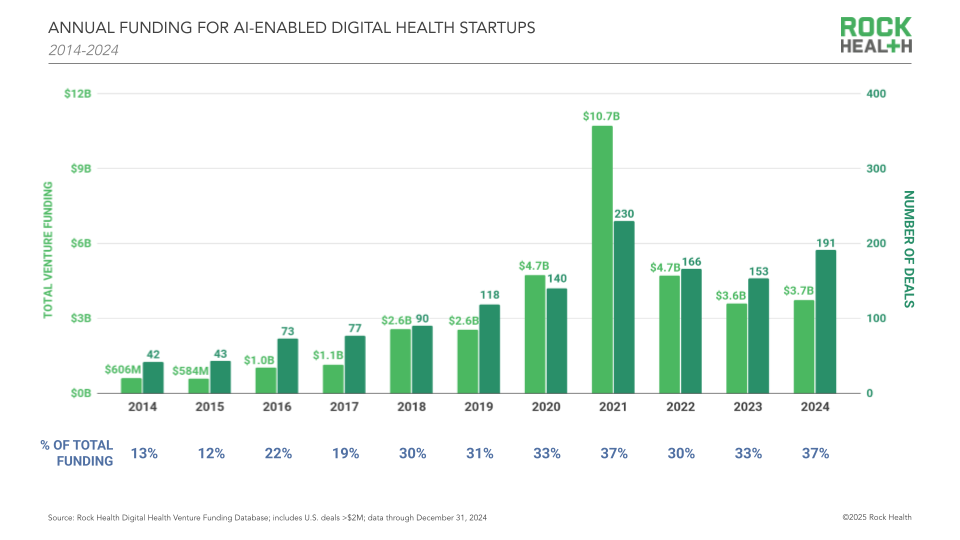

To no one’s surprise, AI enablement continued to sweep investor and enterprise attention in 2024. Funding for AI-enabled digital health startups comprised 37% of the year’s overall sector funding across 191 deals.4

We see concentration happening in the AI space, too—first, among companies developing foundation models (i.e., large-scale models pre-trained on vast data sets that power entire ecosystems of downstream AI applications). Because foundation models are expensive to build and maintain, they’re often built by Big Tech players who can shell out the massive capital needed to acquire data, harness compute power, and deploy staff for model development and management—or they’re the product of open source initiatives. Foundation models are so integral to healthcare AI that we call them the elephants LLMs in the room.

There are also digital health companies building upon these foundation models to develop enterprise tech stacks, an application layer with its own share of concentration. Goliaths in this space are incumbent software providers like Epic and Cerner, healthcare divisions of Big Tech players like Microsoft, and digital health companies that have raised enough capital to compete like Commure and Abridge. These companies have stood up complex AI architectures for large healthcare customers, tend to address multiple use cases, frequently complete custom builds, meet strict compliance and privacy requirements, and often partner with one another.

“While there are many companies in healthcare AI, the seemingly low barrier to entry is a bit of a mirage. Similar to how there are clear leaders at the foundation model level, there are select players who can deliver enterprise-grade AI solutions for major healthcare organizations. The bar for success is as high as ever, with stringent and evolving requirements beyond core product capabilities. That said, the effort and investment is worth it—it’s a huge opportunity to create historic impact.”

– Shivdev Rao, MD, CEO and Co-Founder, Abridge

Though Goliaths command AI foundation models and enterprise-scale builds, there’s still room for smaller startups to grow—but they’ll need to think carefully about their positioning. There will still be demand for AI solutions addressing specialized use cases or those that work with smaller customer segments like independent practices. However, these Davids will need to keep an eye on the Goliaths and their roadmaps—perhaps to work with them or to consider a path to acquisition.

“Historically, small- and medium-sized businesses weren’t perceived as big enough markets against which health tech players could justify standing up a direct salesforce. However, a crop of current healthcare generative AI players have implemented viable go-to-market strategies pursuing ‘down market’ SMB buyers. These buyers want gen AI capabilities, but aren’t top-priority customers for larger IT players, and since gen AI products generally have a lower implementation burden, it’s a win-win opportunity for startups and smaller players.”

– Julie Yoo, General Partner, a16z Bio + Health

Buzzworthy value propositions and clinical indications

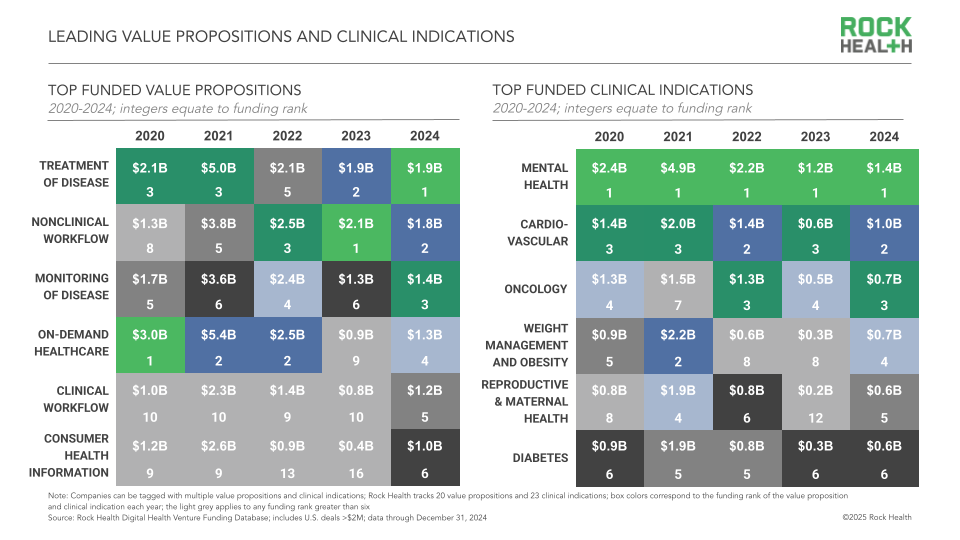

Continuing our exploration of sector concentration, we wanted to understand if funding was concentrating within the “hottest” categories in digital health. To evaluate this, we calculated how much of 2024’s overall funding was represented within the six top-funded value propositions and clinical indications.5 The analysis provided interesting results: in 2024, funding for the top six value propositions of digital health startups comprised 85% of total sector funding—nearly 10% more concentrated than at any point in the past few years. To a lesser extent, we also saw funding concentrated in the six most-funded clinical indications, totaling 48% of sector funding compared to just 28% in 2023.

There are several likely explanations as to why digital health investment is concentrating within these categories—the first being buzzworthy industry activity. GLP-1 excitement put weight management and obesity care on the radar for investors both inside of healthcare and out. There’s also a halo effect for related areas like food as medicine, paving the way for raises including FoodSmart’s6 $200M megadeal last June. Mental health also continued to secure media and investor attention, topping the list of top-funded clinical indications for the sixth consecutive year with $1.4B raised.

Second, there are shared, underlying dynamics tying several of these categories together—think of them as rising tides lifting all boats. Healthcare’s AI revolution is transforming key elements of disease treatment and monitoring, as well as clinical and nonclinical workflow—a boom that is boosting startup raises in each category. Similarly, the comorbidity status of obesity and label expansion of GLP-1s to treat second-order conditions correlates to funding spikes in categories ranging from diabetes to women’s health.

A final driver of capital concentration across value propositions relates to those Goliath dynamics we discussed earlier. Large healthcare customers are looking for vendors that can address multiple pressing needs—this means that the big digital health companies selling to these customers will have to expand across value propositions and therapeutic areas. For example, 2024 saw nonclinical workflow platform Commure dive deeper into clinical workflow with its acquisitions of Augmedix7 and Memora, while surgical workflow software Caresyntax ($180M raised in August) built out administrative and financial capabilities related to operating room management. In 2025, we foresee more digital health Goliaths using acquisitions to weave tapestries of features that address multiple of their customers’ top use cases.

Opportunities big and small

David and Goliath dynamics in digital health came into sharper focus in 2024, aligning with broader venture and healthcare industry trends and reflecting the natural layers within technology stacks. We believe a balance of big and small players will be needed to preserve diversity of thought and innovation in healthcare. For founders and investors, it’s important to remember that not every startup needs to be a Goliath (or unicorn…or decacorn) to be successful. Creating value for customers and maintaining a clear understanding of one’s addressable market, achievable scale, and valuation will help maintain a right-sized perspective.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in building a more equitable future at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnotes

- Calculated using historical annual inflation rates provided by Bureau of Labor Statistics

- We first reported on the rise of unlabeled raises in 2023, which refer to capital raises that are not publicly labeled with a series or round label. Digital health players may avoid publicly attaching labels to weaker rounds to avoid or delay valuation haircuts

- Pitchbook data through December 4, 2024

- We count AI-enabled digital health startups as any solution powered by AI, not just companies selling AI as their core product—e.g., digital health companies that are using AI to improve their existing products in telehealth, remote monitoring, etc., but aren’t vying to be part of an enterprise’s AI tech stack

- Our back-of-the-envelope methodology: We added up the total funding across the top six value propositions and clinical indications then calculated that sum as a percentage of each year’s total funding. One important limitation to this analysis is that startup fundraises can be tagged to multiple value propositions and clinical indications, so their funding dollars may be double counted across multiple categories

- Foodsmart is a Rock Health portfolio company

- Augmedix is a Rock Health portfolio company