2021 year-end digital health funding: Seismic shifts beneath the surface

If you’ve been following our updates, you know 2021 was a (the!) year for digital health venture funding: In July, we reported that the year had already topped all of digital health’s previous annual funding records with six months left to go. While it may feel like old news to share just how momentous 2021 was, our updated funding graphs—with extended axes just to capture 2021’s growth—speak for themselves.

However, beneath the chart-topping numbers are signals of something deeper. 2021’s funding frenzy was, at points, both the cause and effect of bigger shifts within healthcare. Specifically, the sector experienced major changes to its infrastructure, business models, and talent pool that will make downstream effects in 2022 inevitable.

In this piece, we’ll review 2021’s funding environment with a focus on the underlying changes beneath the surface’s venture stats. We’ll place our bets on how the digital health landscape will move throughout 2022—and where there might be tremors ahead.

Recapping a breakthrough year

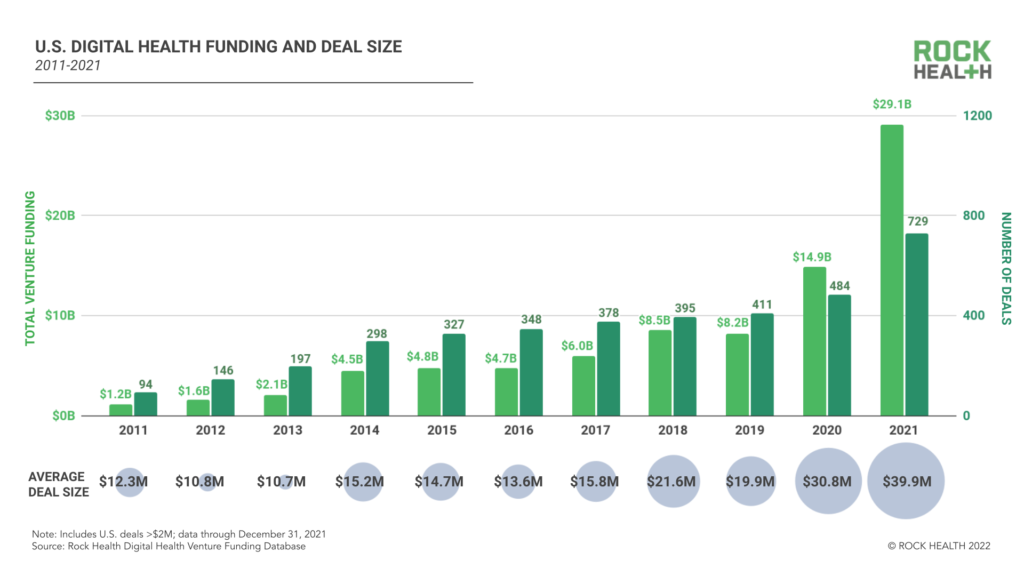

2021’s total funding among US-based digital health startups amounted to $29.1B across 729 deals, with an average deal size of $39.9M. Overall investment nearly doubled 2020’s $14.9B former record haul.

Topline funding growth was driven in large part by 88 mega deals ($100M+ rounds), which brought in $16.6B, or 57% of the year’s total. In terms of deal size, 2021 saw four of the five largest digital health deals since we started tracking in 2011: Noom ($540M), Ro ($500M), Mindbody ($500M), and Commure ($500M).1

In 2021, digital health companies catalyzing R&D in biopharma and medtech topped the chart with $5.8B in funding, stimulated by the COVID-accelerated adoption of real-world evidence and decentralized trials. Investments in digital products supporting disease treatment grew 2.6x between 2020 and 2021 as coverage pathways for prescription digital therapeutics widened. Healthcare marketplaces also experienced a 3.2x year-over-year funding growth, driven by upticks in D2C marketplaces (Mindbody), caregiver marketplaces (Honor $370M)2, and clinical job boards (Trusted Health $149M across two rounds).

Maintaining the top spot, digital health startups offering mental healthcare raised $5.1B, $3.3B more than any other clinical indication in 2021, and nearly double 2020’s funding total ($2.7B). Trends driving investment in this category include the integration of mental health services into broader virtual care platforms (think K Health acquiring Trusst) and the rise of virtual options for intensive mental and behavioral health needs, led by companies like Lyra Health ($200M), NOCD ($33M), and Equip Health ($13M).3 Investors also boosted funding for diabetes care and musculoskeletal (MSK) care, conditions that can increasingly be managed virtually. MSK funding grew six-fold between 2020 ($236M) and 2021 ($1.4B), as virtual MSK clinics Hinge Health ($300M and $400M) and Sword Health ($25M, $85M and $163M) each completed multiple raises across the year.

In previous years, digital health’s pace of venture funding wasn’t always matched by exit activity; but in 2021, outsized funding came with a landslide of exits. 2021 saw an average of nearly 23 digital health exits via merger or acquisition each month, almost double 2020’s monthly average of 12. And while some of the year’s anticipated SPAC deals didn’t materialize, 23 digital health companies went public via SPAC or IPO in 2021, almost triple the previous peak of eight in 2020.

A balanced perspective

As we reported on digital health funding throughout 2021, one of the most common questions we heard from investors, entrepreneurs, and corporate friends was, “Is digital healthcare in a bubble?” Rock Health has been on bubble watch since 2019, when we shared our six-point framework for assessing the health of the venture market. Our take on 2021? The digital health market wasn’t an across-the-board bubble, but it wasn’t placid water either.

First, healthcare isn’t immune to broader economic trends, and 2021 was a historic year for venture funding across industries; U.S. venture capital investment totaled $329.8B in 2021, nearly doubling 2020’s $166.6B. In digital health specifically, 2021’s VC landscape heated up with the participation of new funds and growth firms—including Tiger Global, which participated in 25 digital health deals in 2021 (second only to General Catalyst’s 37). As digital health VC went into overdrive, many startups saw opportunity in these market conditions and raised multiple rounds close together, with 60 companies raising twice in 2021 and two companies raising three rounds within the calendar year.

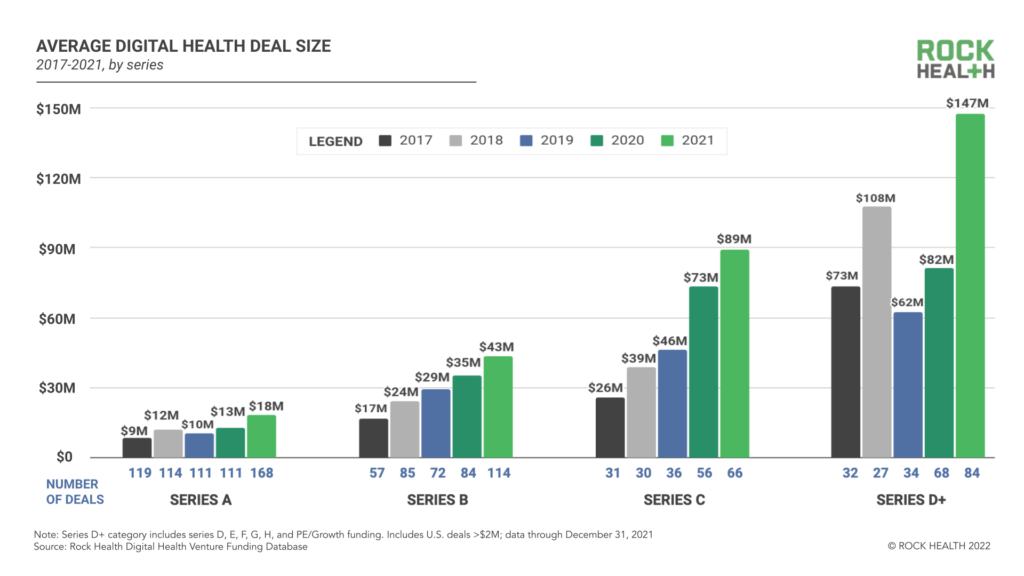

Also in 2021, competition between investors to deploy into early-stage deals (seed, Series A, and Series B) pushed up valuations. From 2020 to 2021, the average Series A round grew 38% to $18M, while the average Series B grew 23% to $43M—just $3M less than 2019’s average Series C. The year also saw a record number of mega ($100M) early stage deals, including ten mega ($100M+) Series B raises and one mega Series A round (EasyHealth). To compare, 2020 had six mega B rounds, and we’ve only seen one other mega Series A since we started tracking funding in 2011 (Insitro in 2018).

2021’s bullish early-stage behavior may impact Series C and D activity in the next 18-24 months. As today’s A and B companies mature into later rounds, they could feel pressure to sustain growth that validates the “extraordinary” performance and revenue goals priced into early-stage valuations; this could trigger some down-rounds or series extensions as companies begin to adjust expectations. However, we have seen companies (including within our own portfolio) exceed pre-pandemic projections by wide margins; one could argue that, for the most promising companies, today’s valuations aren’t too high but that historical benchmarks are too low for the accelerating digital health market.

“Early stage investors are so focused on getting into digital health deals that they’re coming in hot at Seed, Series A, and Series B and setting high valuation bases. A rationalization happens around Series C when investors are forced to scrutinize the company’s revenues and real business model.”

– Michael Matly, MD, Co-Founder and Managing Partner at 111° West Capital

There are a few signs pointing to continued acceleration in the digital health market. First, digital health adoption appears to be stabilizing at a ‘new normal’ following the onset of the COVID-19 pandemic. According to Rock Health’s 2021 Digital Health Consumer Adoption Survey,4 73% of telemedicine users expect to continue using telemedicine at the same rate or higher in the future. We’re also seeing providers continue to offer virtual care options. Eighty percent of Rock Health Consumer Adoption Survey respondents with a primary care provider (PCP) said their PCP offered telemedicine in 2021, nearly double the 44% who said their PCP offered telemedicine prior to the pandemic. And, according to research from EY, 60% of physicians plan to continue offering care through telemedicine even after the pandemic.

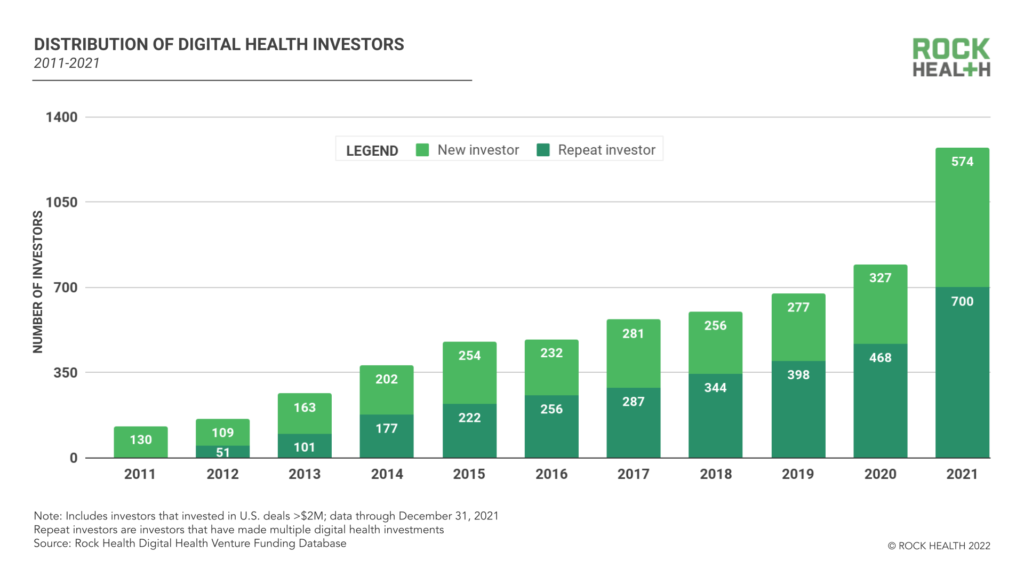

We also see macro signals that the investor community is settling into a long-term funding stride for digital health. There remains a healthy mix between new (45%) and repeat (55%) investors in the sector, balancing new cash with the consistent behavior of industry experts. Rounding out the diverse mix, big tech players are investing and acquiring in the space, joined by a growing number of middle children—smaller-but-still-sizeable retail and tech companies like Best Buy that are increasing their forays into digital health.

A final signal of market maturation is the growing rate of digital health exits. Over the past decade, roughly one in four (23%) digital health dollars invested has gone to companies that ultimately exited; 13% of those funds went to companies that merged or were acquired, while 10% went to companies that exited onto the public markets. For comparison, when we last reported on sector liquidity in 2019, only 15% of digital health’s investment dollars had exited.

Provided that public market volatility remains manageable, we expect digital health’s exit pace to stay hot. 2021’s substantial Series D+ raises (1.8x growth in the average Series D+ check size between 2020 and 2021) provide a rough estimate of companies that might be shoring up for IPO roadshows and SPAC pipe fundraising in the near future. For new entrants, this “senior class” of digital health companies offers a real-time playbook for go-to-market strategy and building market share.

Forces of change

Beneath increased investment, sustained growth in consumer adoption, and a quickened exit pace, we believe there are three forces at work reshaping the digital health sector from the ground up: improved infrastructure, nimble business models, and a war for talent. Each of these forces underwent a major evolution in 2021 that will make change in 2022 inevitable.

Infrastructure buildout

Historically, the fragmented nature of the U.S. healthcare system made it nearly impossible for players to share data for things like coordinated care, billing, or research. Companies had to build and manage their own tech stacks from scratch or fit into the mold of pre-existing EMRs.

However, as digital health’s platform wars heated up in late 2020, major healthcare and life science companies experienced firsthand the headaches of merging different data silos during partnerships or acquisitions—often implemented under pandemic-induced duress. Regulators pushed for increased patient transparency, which required health systems and payers to make their data more user-friendly. Plus, falling prices for data storage and computing power made favorable conditions for outfitting digital health with a new set of “pipes.”

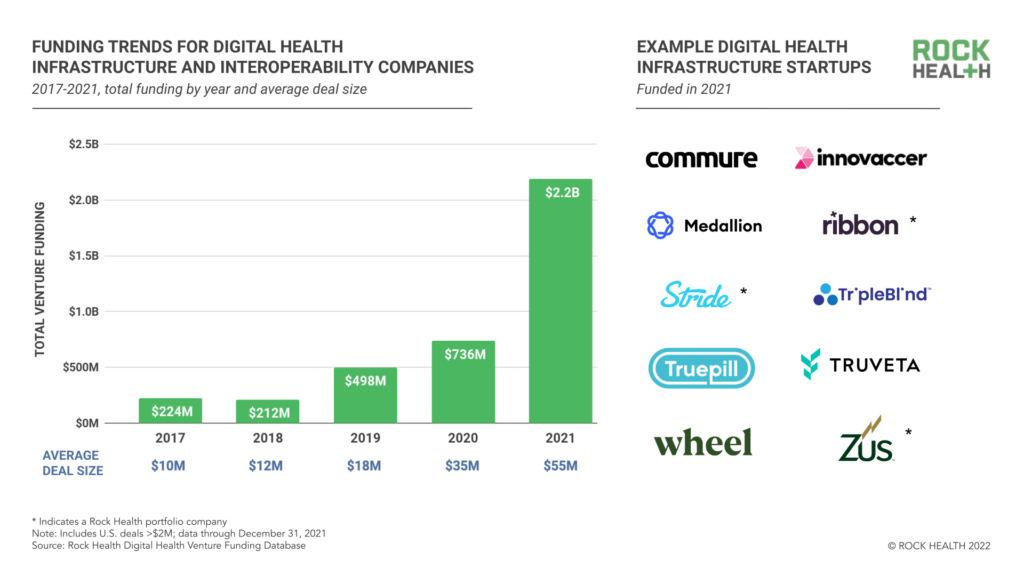

In 2021, digital health infrastructure and interoperability startups secured $2.2B across 40 deals in 2021, nearly 3x 2020’s dollars invested in the category ($736M). Today’s infrastructure landscape includes companies like Innovaccer ($105M), Redox ($45M), and Ribbon Health ($43.5M) that integrate data streams into unified API ecosystems, while TripleBlind ($8.2M and $24M) and Truveta ($95M and $100M) enable cross-company data analysis. ScienceIO ($8M) and Centaur Labs ($15.9M) streamline data structure and labeling, while Commure, Truepill ($142M), Wheel ($50M), and Zus Health ($34M) offer “LEGO kits” or building blocks for others to get digital health solutions up-and-running.5

“Infrastructure as a service used to be a boring market in digital health. Now, as virtual service providers mature and consolidate into platforms, we’re seeing a big opportunity for behind-the-scenes players that focus on interoperability and data sharing.”

– Missy Krasner, Venture Chair at Redesign Health

We see this growing cohort of infrastructure players pushing the market forward in three big ways. First, they lower upstart barriers for new digital health companies and free up founders to focus on non-technical differentiators—clearing the way for new patient-centric digital health approaches in the future. Second, they reduce friction and cost for digital health integrations, mergers, and acquisitions, accelerating the platform wars and industry consolidation. Third, they contribute to a unified industry data ecosystem, unlocking new possibilities in population health, a segment we’ll be watching closely in 2022.

Nimble business models

As the most severe portions of the pandemic subsided in 2021, healthcare sales cycles returned to pre-pandemic timelines and point solutions faced more trouble proving out differentiated value to overwhelmed buyers. In certain sectors like telehealth, startups found themselves in commodity businesses, winning enterprise customers not with product quality but with network scale and integration capabilities. Changes like these are pushing digital health companies to reconsider their business models and go-to-market strategies.

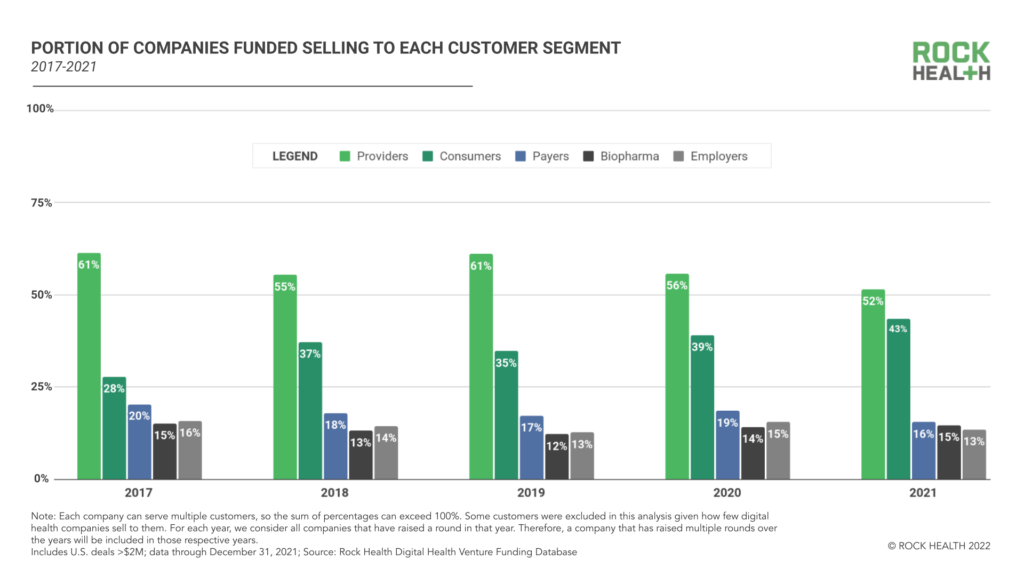

As we alluded to back in July, 2021 reached a new peak for direct-to-consumer (D2C) healthcare. D2C-only players accounted for 24% of total digital health funding in 2021, while 43% of companies that raised in 2021 served consumers as a customer segment—setting two new records for the sector.

2021’s rise in consumer healthcare is driven in part by the nationwide rise in out-of-pocket healthcare spending. In 2021, 51% of the US workforce enrolled in high-deductible health plans, and annual out-of-pocket spend grew to $500B. Companies looking for a greater share of consumer dollars launched multi-feature virtual care hubs (Hims & Hers, Cue+), leading investor Chrissy Farr to proclaim, “every digital health startup is a clinic now.” Other D2C health players began leveraging their user bases to negotiate enterprise contracts and subsidize consumer costs—think Peloton striking deals with health plans and employers—in an approach a16z’s Julie Yoo calls B2C2B.

2021 also saw healthcare startups expand across product categories and step into complex care delivery. Ro ventured into weight management and fertility, Headspace moved beyond mindfulness into talk therapy, and Carbon Health launched a pathway to transition patients to higher acuity care. Expansion mindsets also pushed digital healthcare players into brick and mortar, as Thirty Madison opened its first Keeps location, Tia raised $100M for clinic buildout, and digital MSK provider Kaia Health inked a partnership to offer in-person physical therapy. Omnichannel shifts happened in the opposite direction too: UnitedHealthcare, Cigna, CVS/Aetna, and other payers launched virtual-first products, and Amazon’s Alexa entered hospitals and senior living centers. To us, 2021’s moves reinforce that healthcare isn’t destined to be virtual-only. Rather, it will combine digital and in-person touchpoints to strike the right balance of accessible, high-value care.

Lastly, 2021 saw a leading cohort of digital health companies forgoing fee-for-service models and moving toward value-based care. Value-based care models encourage providers to utilize any range of physical and digital approaches to deliver quality care at reduced cost. While 2021’s top digital value-based care news was Oak Street Health acquiring RubiconMD, virtual care managers Pomelo Care ($8M) and Thyme Care ($22M), as well as medication manager Arine ($11M)6, all raised with value-based care models at their core.

“We’re seeing slow but steady movement toward value-based payment, and this shift will probably be accelerated by legislative action. Technology startups have big roles to play here by enabling efficiencies for organizations entering value-based arrangements.”

– Andrey Ostrovsky, MD, Managing Partner at Social Innovation Ventures

We expect digital health’s value-based care transformation to extend well into the new year. While many of today’s value-based programs target Medicare and Medicare Advantage, commercial plans and Medicaid (whose enrollment grew 15.5% from 2020-2021) might be next. We’re also interested to see if value-based care’s popularity will secure funding attention for upstream interventions in social determinants of health, preventative medicine, and primary care—especially if moves from the K Health-Anthem-Blackstone joint venture Hydrogen Health are any indication. Lastly, because value-based contracts are so dependent on outcomes reporting, we expect to see more investments in patient data capture and analytics to prove out both clinical and business returns for value-based care models. As early signals, Spring Health ($190M) and Omada Health7 both launched outcomes data initiatives in 2021. Stay tuned, as we predict more focus on outcomes reporting in 2022.

“At Arine we say, ‘We deliver on outcomes.’ It’s our commitment to our investors, our clients, and to patients that we deliver on ROI at scale and address health outcomes at scale. When our metrics demonstrate clear value to the topline/bottom line and to quality of care, then incentives are aligned.”

– Yoona Kim, Co-Founder and CEO at Arine

Talent wars

Plentiful capital, building block infrastructure, and expanded business models are enough to get any founder excited about making healthcare massively better. But there is one snag…we’re running out of people.

The Great Resignation hasn’t left healthcare unscathed, and the interdisciplinary nature of digital health compounds its vulnerabilities. Digital health companies need strong software engineering and product teams, as well as strategic guidance from healthcare leaders who have been around the block. Not to mention, digital health players delivering care need to compete with the broader healthcare industry for clinical talent and caregiver staff—a cohort of employees that are just plain burned out.

In an indirect manner, digital health’s buzzing investor activity might also be feeding into the industry’s talent war. Investor-heavy rounds, especially in early stages, take equity off the cap table that could otherwise incentivize new employees. We might see some pushback in early stage funding rounds as founders start safeguarding equity from investors and using it to attract competitive hires—even at the expense of building up their war chests.

For clinical roles, 2021’s talent shortage was particularly pronounced. Career stress, exacerbated by the COVID-19 pandemic, pushed a greater number of clinicians to consider leaving medicine at the same time that non-traditional healthcare employers began hiring physicians and ramping up clinical roles. For digital health companies in service delivery (calling all virtual clinics), clinical talent may be a rate-limiting factor for growth.

To address these clinical talent gaps 2021 saw several digital health startups offering creative approaches. Capital flowed to on-demand clinical staffing marketplaces including Prolucent Health ($11.5M), connectRN ($76M), Nomad Health ($63M), and ShiftMed ($45M). MedArrive raised $25M to tap into clinical staff when they’re being underutilized, while infrastructure player Wheel heralded the need for virtual clinics to adopt dynamic staffing models in order to manage variable demand. Some virtual care offerings like Seven Starling ($2.9M) adopted one-to-many care models to maximize provider capacity, while Omada, Noom, and Robin ($2M) promoted support-driven care programs led by coaches or peer leaders rather than relying on licensed clinicians—and began to prove out evidence-based outcomes from this approach.

The winning companies in today’s digital health’s talent wars will be those that either find ways to expand their talent pools (cue more partnerships and M&A), creatively extend staff through emerging care models and technologies (e.g., AI / ML), or make themselves so attractive that employees compete to join the team—or, better yet, apply a combination of these three strategies. We also expect digital health startups to beef up hiring packages to attract clinical and nonclinical talent, which could redefine the healthcare job market with new perks and flexibilities, including higher salaries and remote or hybrid arrangements. As talent becomes a differentiating factor for company growth, consider this as a “calling all nerds” moment: for those interested in making the jump to digital health, the best time to do so might be right now (and hey–we’re hiring!).

“In digital health today, it’s harder than ever to recruit great people, it’s harder to hire for scale, and it’s especially hard to find those leaders who bring a depth of expertise in any specific area of focus. As a result, startups are making bigger investments to find people. Good founders understand the value of having the right people around them and they’re willing to pay for it.”

– Tim Gordon, Founder and Managing Partner at Aequitas Partners

2022: The year of disciplined innovation and execution

2021 was the biggest year for digital health investment, bolstered by never-before-seen infrastructure tools and business model options. The past twelve months have taught us that when capital isn’t a constraint, execution is all that’s left. Companies that take in capital without investing in infrastructure, business model innovation, or talent and leadership are headed for tough future quarters to meet the expectations that come with high valuations.

Within the next five years, we’ll be writing case studies on what today’s digital health leaders did in a buoyant market. In the near term, we’ll be watching to see which of our 2022 predictions pan out. But 2022 isn’t the end of the horizon. Companies that seize this moment to execute on business fundamentals and grow alongside the evolving digital health landscape are paving their runways for success—and most importantly, making healthcare massively better.

Rock Health’s venture fund continues to invest in entrepreneurs bringing unique and innovative technology to healthcare. We would love to hear from you. Get in touch!

Rock Health Advisory provides guidance on digital health strategy, access to proprietary funding databases, and in-depth perspectives on the digital health market. For digital health insights targeted to your needs, drop us a note at advisory@rockhealth.com.

Finally, stay up to date with the latest headlines in healthcare technology and Rock Health news by subscribing to the Rock Weekly.

Footnotes

- Other top digital health funding deals include Peloton’s $550M raise in 2018.

- Honor is a Rock Health portfolio company.

- Equip Health is a Rock Health portfolio company.

- For the past seven years, Rock Health has conducted a survey of U.S. adults ages 18 and over to gauge their utilization and preferences related to digital health solutions. This year’s insights piece, co-published with Stanford’s Center for Digital Health, was based on a survey of 7,980 U.S. adults. Please reach out to Rock Health Advisory (advisory@rockhealth.com), which serves large companies and Fortune 500 corporations, for more information regarding access to this data or for custom analysis for your organization.

- Ribbon Health and Zus Health are Rock Health portfolio companies.

- Arine is a Rock Health portfolio company.

- Omada Health is a Rock Health portfolio company.