H1 2024 digital health funding: Resilience leads to brilliance

It’s been a rocky few quarters, but the digital health sector is resilient—and we’re seeing measured momentum in funding and exits to prove it. If H1’s investment pace continues, 2024 funding dollars and deal counts could exceed 2019 and 2023 historicals, two years that serve as helpful comparators outside of the pandemic-fueled funding cycle from 2020 to 2022. Early-stage checks are growing, the proportion of unlabeled deals1 is tapering, and the digital health IPO market is showing early signs of life. Meanwhile, digital innovation in healthcare continues to march forward, with AI attracting even more attention and contributing to funding patterns across product categories and therapeutic areas. Read on for our take on H1’s digital health investments, acquisitions, and public exits.

Early-stage energy

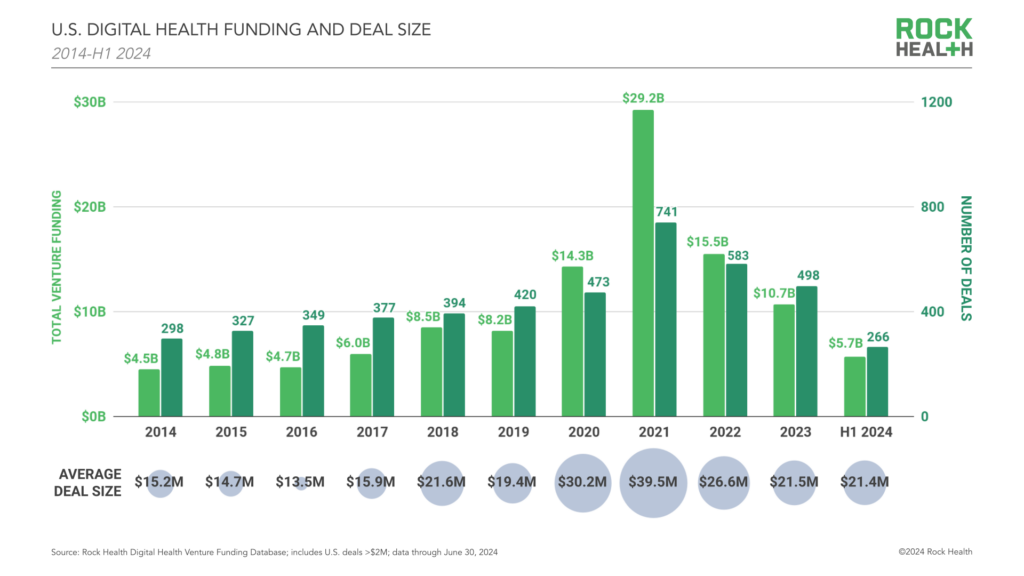

In H1 2024, U.S. digital health startups raised $5.7B across 266 deals. If investment patterns continue, 2024 could exceed 2019 and 2023 year-end totals ($8.2B and $10.7B, respectively).

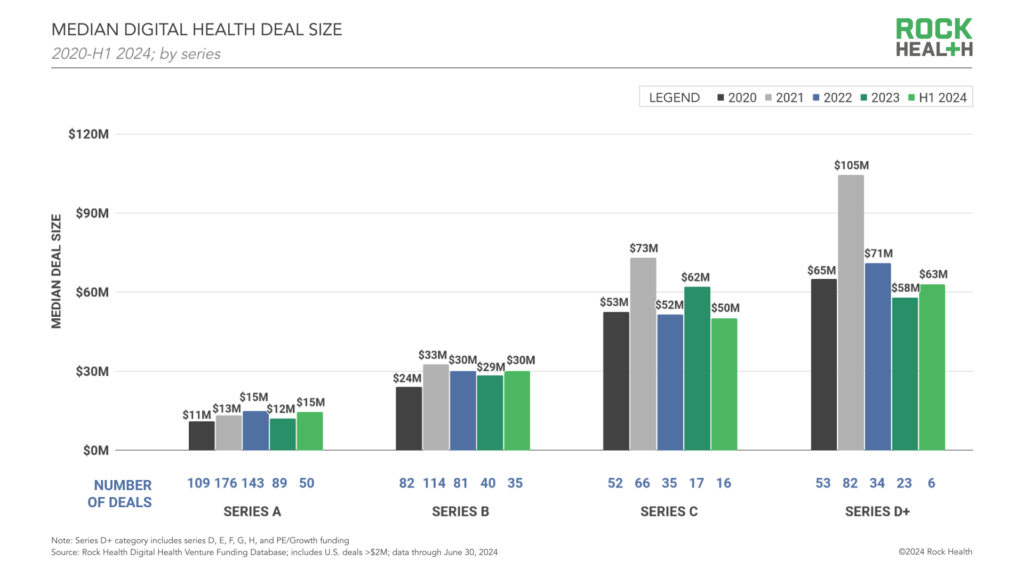

Most of H1’s energy came from early-stage deals: Seed, Series A, and Series B checks accounted for 84% of labeled raises in the half. Series A activity was especially strong in H1, with a median deal size of $15M in the cohort, $3M larger than the median Series A in 2023. H1’s Series A stats were pulled up by double- and triple-digit A raises from startups like precision medicine player Zephyr AI ($111M Series A in March), continuous glucose monitoring platform Allez Health ($60M Series A in May), and AI-powered care enablement company Fabric ($60M Series A in February).

For early-stage startups using AI (38% of digital health companies that raised A rounds in H1 2024 were AI-enabled), big Series A rounds can help support AI upstart costs like training models or acquiring datasets. For others, large As open doors for unique early-stage opportunities like making acquisitions—take Fabric’s purchase of virtual care solution MeMD from Walmart’s shuttered healthcare business in June.

“The Series A pipeline is quite strong right now, and these early-stage rounds can feel like cleaner deals because they don’t have valuation overhangs.”

– Cheryl Cheng, Founder and CEO, Vive Collective

Unlabeled rounds begin to wane

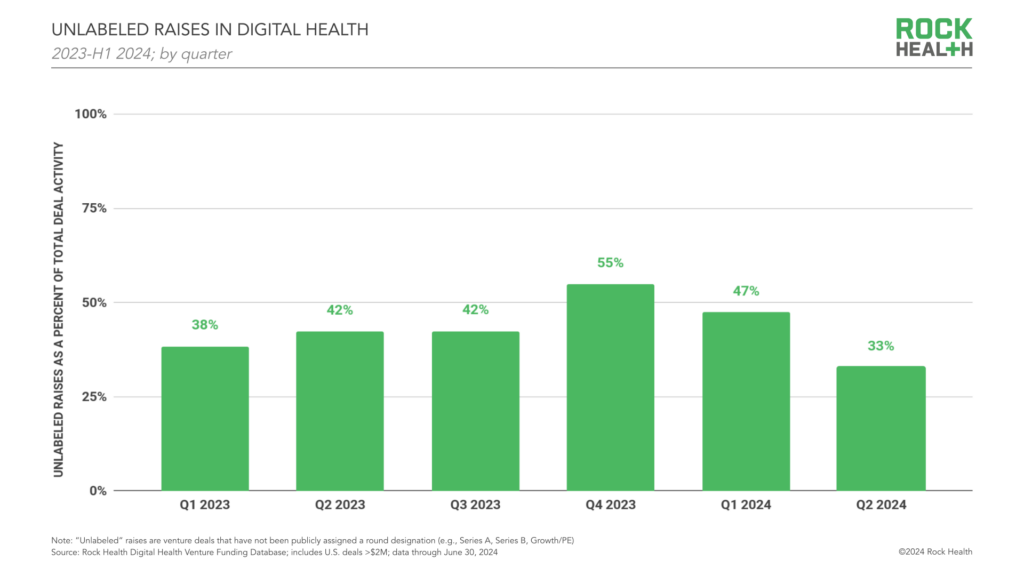

For the past few quarters, we’ve been tracking the percentage of startups raising unlabeled rounds. Unlabeled rounds tend to spike during periods of transition between market conditions, when startups need access to capital but don’t meet benchmarks for their next labeled raise and/or are trying to delay tough conversations on topics like valuation.2 We first noticed a rise in unlabeled deals in early 2023, as the funding environment began to shift away from the COVID-19 public health emergency—overall, 44% of 2023’s digital health deals were unlabeled. The trend continued into 2024, with 40% of H1 2024’s sector fundraises (107 deals) not assigned a series label. Comparatively, 22% of deals were unlabeled in 2022, 19% in 2021, 7% in 2020, and 4% in 2019.

Looking quarter-over-quarter from Q1 2023 to Q2 2024, the prevalence of unlabeled deals has started to taper. Q1 and Q2 2024 showed a decline in percentage of raises that were unlabeled (47% and 33%, respectively) from a peak of 55% in Q4 2023. This waning could mark the beginning of our return to a “more normal” cadence of labeled raises, something we predicted for 2024.

Twenty-four percent of H1’s unlabeled raises (26 deals) were made by startups that had raised an unlabeled round previously. Raising two unlabeled rounds in a row—an extension of an extension of cash runway—could mean that a company hasn’t been able to reach growth benchmarks or profitability. In these situations, down rounds or closures could be on the horizon.

VPs, CIs, and AI (oh my!)

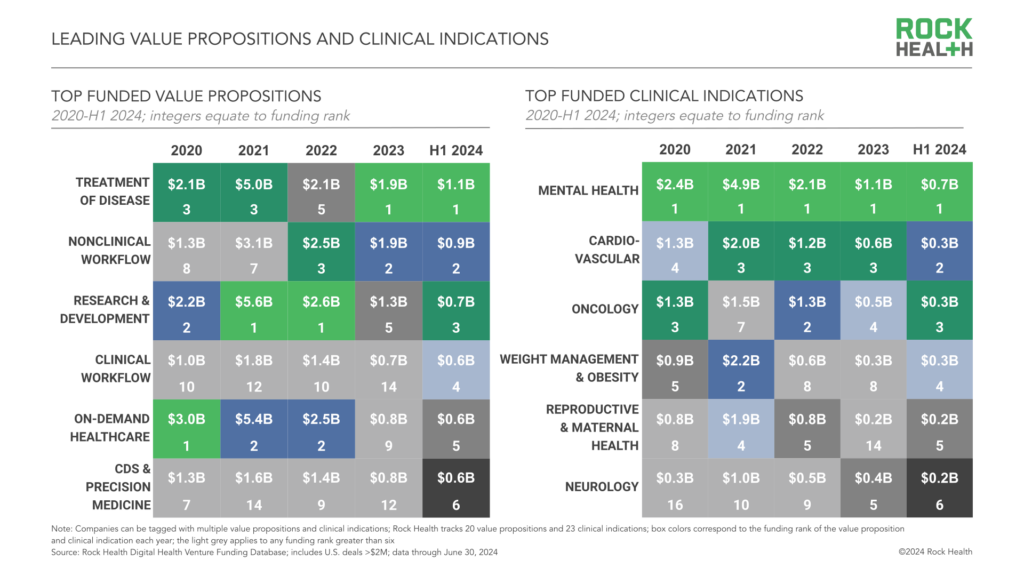

In the earlier days of digital health, investors had their sights and dollars set on funding on-demand healthcare tools, many of which centered on telemedicine. While on-demand healthcare is still a central part of digital health (and H1’s fifth-most funded value proposition for digital health startups), today’s investors are supporting a much more diverse mix of solutions informed by consumer trends, market trends like commoditization and specialization, and of course, AI. One in three dollars invested in H1 (34% of total sector funding) went to digital health startups leveraging artificial intelligence—which helped to shape the rankings of digital health’s top-funded value propositions and clinical indications this half.

Treatment of disease grabbed the top funding spot by value proposition, with food as medicine startup for chronic condition care Foodsmart’s $200M raise3 feeding the $1.1B total. AI momentum underpinned deals in categories next on the list, including nonclinical workflow ($896M), R&D for pharma and medical devices ($737M), and clinical workflow ($639M).

“AI is helping us combine multiple parts of the care journey, across all care experiences. In the future, benefits navigation, clinical guidance, and care delivery won’t be delivered by separate companies or point solutions within the healthcare ecosystem. They’ll be features that work in concert within products, and they’ll happen in under 90 seconds for a seamless patient experience.”

– Glen Tullman, CEO, Transcarent and Managing Partner, 7wireVentures

Mental health again topped the list of top-funded clinical indications in digital health with $682M raised in H1 2024, while headlines in weight management and obesity care bolstered funding to startups in the category ($261M).4 Investments in companies developing menopausal and pelvic health5,6 solutions bumped H1 funding for reproductive and maternal health to $214M.

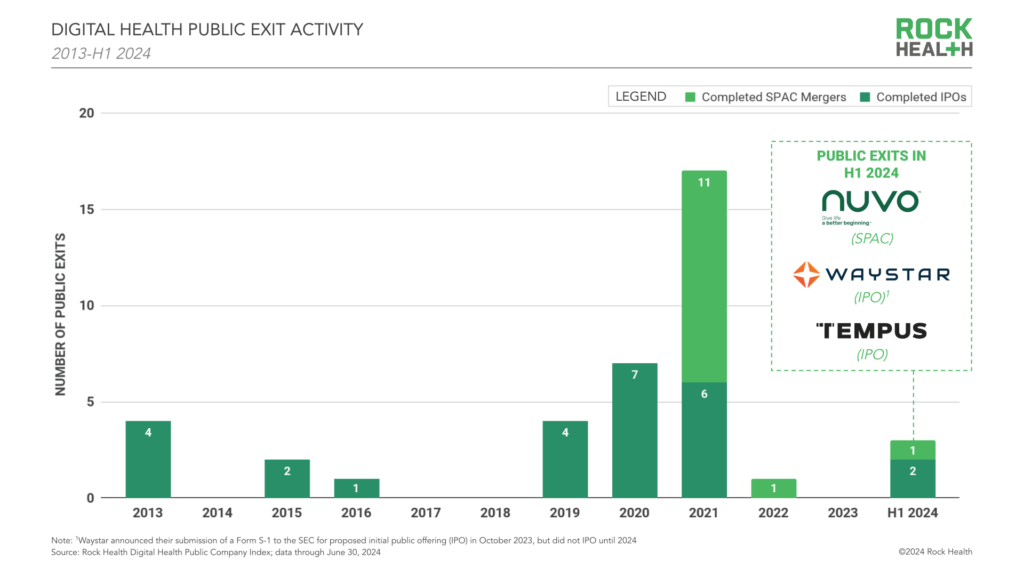

Signs of life in the exit markets

After 21 months without a public exit, Q2 2024 saw three digital health companies exit onto the Nasdaq or NYSE: remote fetal monitoring platform Nuvo (public exit via SPAC in May 2024), revenue cycle management company Waystar (IPO in June 2024), and precision diagnostics player Tempus AI (IPO in June 2024). This activity mirrors a modest IPO uptick in the broader markets, as well as natural forward movement for some late-stage digital health companies.

Waystar and Tempus AI’s IPOs in particular give us important intel into the perspective of late-stage digital health players weighing exit possibilities. For one, debt management is a key consideration. Both Waystar and Tempus disclosed that funds raised during their IPOs would be used to pay down debt in a high interest rate environment. Aligning exit price to 2024’s economic climate is also top of mind. Tempus, for example, priced its IPO at a nearly 40% discount from its $10.25B valuation set in 2022.

For digital health players not planning public debuts, there may be opportunities to be acquired, though buyers are more selective in today’s market. Digital health companies—the top acquirers of other digital health companies—are facing pressure from investors and board members to act conservatively, and acquisitions could be perceived as expensive distractions. As a result, acquisitions of digital health companies by other digital health companies have dropped, clocking in at 34 deals in H1 2024, less than half of 2023’s total (83 deals).

“There are many good companies trying to get bought, but it’s hard to make those deals work. Even if they are interesting companies, potential buyers are focused on their immediate priorities. Anything that is not directly related to what we are trying to get done is de-focusing and incredibly risky.”

– Joanna Strober, Founder and CEO, Midi Health

Though overall acquisition activity has fallen, private equity (PE) has taken a larger role in digital health M&A so far this year. PE firms acquired 10 digital health startups in H1 2024, more than the total number of digital health acquisitions they made in 2023 and on track to surpass respective totals from 2021 and 2022. PE firms do rigorous diligence and historically favor companies with established business models—and profit. Even digital health companies in tight financial situations can pass the PE sniff test, as long as they have clear business models and opportunities for operational improvements that lead to growth.

Resilience leads to brilliance

The digital health sector continues to demonstrate resilience and adaptability. Funding momentum (especially at the early stage) and the tapering of transition measures like unlabeled rounds hint that we might be returning to more “normal,” sustainable venture patterns. Big questions still loom on the horizon—like how the U.S. presidential election will shake out, what will happen to virtual care flexibilities, and which digital health roles retailers will ultimately choose to play. Yet, the first half of 2024 proved that digital health founders and investors have their eyes on the prize, which gives us confidence in what’s to come.

Tap into insights and strategic guidance for enterprise companies with Rock Health Advisory.

Get in touch with the venture team at Rock Health Capital.

Join us in building a more equitable future at RockHealth.org.

And last but not least, stay plugged into the Rock Health community and all things digital health with the Rock Weekly.

Footnotes

- “Unlabeled round” is a term we first used in our H1 2023 report to refer to capital raises without associated round labels (e.g., Series A, Series B)

- Unlabeled rounds tend to be raised as convertible notes or SAFEs in order to defer questions about valuation adjustments until the next labeled round

- Foodsmart is a Rock Health portfolio company

- Rock Health first started tracking venture funding for startups that support weight management and obesity care in H2 2023; companies tagged as delivering weight management and obesity care have all prior fundraises tracked within this category

- Sword Health offers pelvic condition support through its Bloom program

- Sword Health’s round was publicized at $130M, but consisted of a $100M secondary share sale and a $30M primary share sale; Rock Health only tracks primary share sales (a.k.a. primary rounds) in its Digital Health Venture Funding Database